3 Places You Must Save and Invest Your Income

Key Points:

- The 3 principles of investing: risk-reward, compound interest, and time in the market.

- Invest in: emergency fund, employer retirement plan, tax-advantaged accounts.

- Index funds present the best risk-reward balance for the majority of investors.

You’ve been working hard and have built a nice little nest egg. But what do you do with all this cash to put it to the best use? With inflation nearly hitting double digits in much of the Western world, we must be savvy if we are to mitigate this inflationary damage and allow our money to work for us.

This article will cover the most critical questions regarding what to do with your money to put it to good use while keeping it safe. There is no get-rich-quick scheme here, and if you are looking for high-risk, high-reward investments, this is not the article for you.

When it comes to savings and investments, slow and steady are always best. While it won’t make you rich overnight, it will build significant wealth over time, with the benefit that you can set it and forget it.

Investing Can be Complicated

Investing is often a financial minefield of overly technical jargon and curious advice from “experts” with questionable motives. With so many investment vehicles, from savings accounts, managed funds, ETFs, equities, bonds, and everything in between, trying to find a simple yet effective solution can feel like pulling teeth.

For those who are not financial experts, trying to profit from individual stocks and options is akin to gambling. It may work when the stock market is going up, but it is only a matter of time before it all comes crashing down.

Many, including myself, have been burned by poor stock choices, which they were told would be a “sure thing”. Thousands have lost out due to FOMO (Fear Of Missing Out) from the recent cryptocurrency and tech crash.

These people might be tempted to stick their cash under their mattresses or buy physical commodities such as gold and silver where they can physically see their wealth.

Unfortunately, the stock market will almost always outpace cash and commodities, at least for the regular investor. Love it or loath it, the stock market is one of the best ways for a regular Joe to make money.

Fortunately, investing doesn’t have to be complicated, or risky. Just a few simple practices will turn your hard-earned cash into as close to a risk-free return as is possible.

Risk Vs. Reward

Three fundamental principles must be understood before investing. The first is that return on investment and risk are most often inversely correlated. High-reward vehicles, such as Real Estate Investment Funds (REITs), can yield a tasty 10-15%, but they are considered higher risk and volatile.

On the other hand, savings accounts are as close to risk-free as is possible, with most accounts insured by the state. For example, the U.S. FDIC insures individual savings accounts up to $250,000. Unfortunately, this safety is offset by a poor interest rate of around 0.16% as of October 2022, although this is expected to rise as the Fed increases U.S. interest rates.

Generally, the higher the reward, the higher risk. And while a higher risk may be acceptable for the money you can afford to lose, it certainly isn’t for cash we are banking on to buy a house or build a retirement fund.

Many focus on the reward more than the risk and let their greed get them into trouble. The amount of risk you can tolerate depends on your goals, and how much you could afford to lose.

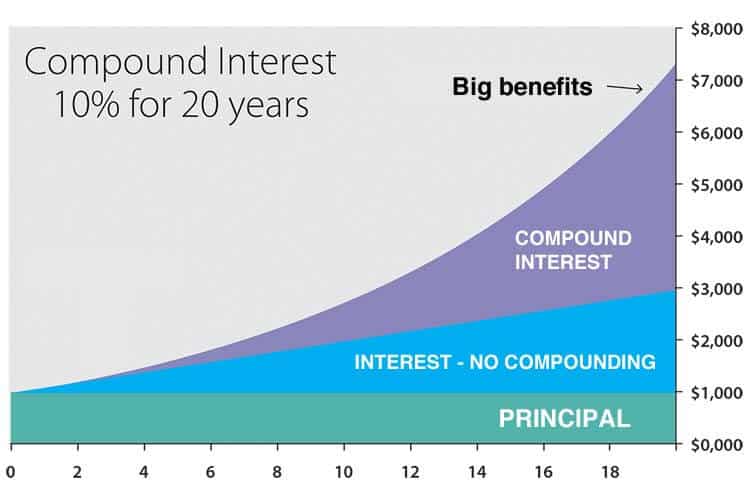

Compound Interest is King

The second principle is that you should always invest in a channel that offers the benefit of compound interest. Einstein once quipped that “compound interest is the eighth wonder of the world”. It is the fundamental principle used by the wealthy to make their money work for them.

Compound interest is the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest. It is the result of reinvesting interest, rather than paying it as dividends, so that interest in the next period is then earned on the principal sum plus previously accumulated interest.

It may sound complicated, but any investment that earns you interest, which is then reinvested to earn further interest, is compounding. This is why holding commodities such as gold, art, and classic cars will rarely meet the returns that the stock market will long-term; commodities are essentially another bet that their value will rise.

There is no income aspect to commodities, so when their value drops, you lose. Compound interest, on the other hand, still generates earnings even when its value decreases (you still always earn interest unless your initial sum goes to zero). When the principal value decreases, you are still building wealth.

Patience is a Virtue

Thirdly, it is imperative that you invest for the long term and do not get greedy. There is almost no reliable get-rich-quick scheme that is inherently safe. Yes, some get lucky, but for reliable results, compounding offers the only guaranteed way to build wealth. This is the basis of all pension and retirement funds.

Many start investing with good intentions but get scared when the market flounders, panic, and sell. The investment vehicles I will show you, however, depend on keeping your money in the stock market when times are both good and bad. It relies on the historical notion that the stock market always rises over long periods (decades).

You need to prepare yourself for the fact that your investments will ebb and flow with the market in general. Some years you will lose, others you will win. But you will always win in the long term because of the tried and tested effects of compound interest.

The Three Fundamental Savings Vehicles

There are three key investment vehicles everyone should utilize, no matter the country. Only after maximizing these three investments can one justifiably spend on luxuries and frivolous purchases.

Your Free Book is Waiting

You’ll Learn:

- How to Create Habits – The Right Way

- Create a Bulletproof Plan to Achieve Your Goals

- Master the Art of Failing

- Rediscover Your Love of Learning

- Instantly Become More Personable

1) Emergency Savings Fund

Firstly, you should place all available disposable income into acquiring six months of living expenses to create an emergency fund. This is preached by many but practiced by few. And in times of viral pandemics and looming recessions, jobs will be lost overnight. Reserving funds for unexpected moments will prove lifesaving.

Living expenses differ by circumstance – a family of four will have much greater living expenses than a single person. Living expenses include monthly housing costs, food, health care, utilities, transport, and debt.

Some claim it should be six months’ salary, but the very minimum should be six months of expenses; that is, you should be able to live for six months if the worst were to happen and you had zero income.

Six months is enough time for most to get back on their feet. For me, this amounts to $16,000. This contingency fund allows for any unforeseen and sudden changes to your living situation, such as a medical emergency or loss of a job.

This money should be highly liquid (accessible as cash at any moment), ideally in a savings account. Interest rates on these are typically low, often lower than inflation, but it is instant access that is the priority – interest is a bonus.

A savings account in this economic climate might earn less than 1% interest annually and not even keep up with inflation, which tends to run between 2-3% a year (in normal conditions).

You may even have to pay taxes on your meager 1% earnings. However, anything is better than the 0% it earns as cash or going into credit card debt, which averages around 20% interest.

Remember, the sole point of this cash is to have instant access to six months of living expenses in case of an emergency, providing not only financial support but mental confidence in your financial position.

A savings account, despite measly returns, also abides by our first investment principle – always invest your money where it can benefit from compounding interest.

Once this emergency fund has reached the six-month mark, as determined by your situation, you can stop contributing to it and simply leave it there to collect interest and be available at any moment.

2) Workplace Pension/Retirement Schemes

Once you have reached your emergency fund target, the next place to put your money is into any workplace retirement scheme.

Always max out your workplace pension offered by your employer. This differs by country and type of job, but if it is available, max it out. If you don’t have this option, it may be worth hunting around to see if any other similar jobs would provide it. It is such a huge bonus.

In the UK, it is now mandatory for all employers to offer a pension plan to employees. The legal minimum that must be paid into a pension is 8% a year of qualifying earnings, of which at least 3% must be paid by the employer.

The usual split is 5% from employees and 3% from employers. This means by investing 5% of your salary, your company will top up your pension contribution by an additional 3%.

This extra 3% is free money and should be maximized. As a bonus, this contributed money usually comes out of your pre-tax income (in the UK), effectively boosting your contribution even further. To not capitalize on this is wasteful.

In the US, a similar system is used in the form of a 401k, except the employer is not mandated to contribute any percentage. The average US 401k contribution is around 13.9%, including the employer contribution. Experts recommend saving 15% of your monthly income towards your retirement fund, although this will likely increase as inflation takes hold.

It is worth noting that if you are self-employed, there are options available to you as well, such as a solo 401k or a SIPP in the UK. Although there is no employer to match contributions, there are at least tax advantages to them. Whatever your employer offers, make sure you contribute enough to receive the maximum employer contribution.

3) Tax-Advantaged Savings/Investment Accounts

Once you have set up your emergency fund and maximized your workplace pension contributions, the third investment stream should be a personal investment vehicle capitalizing on any tax-advantaged accounts your country may offer.

In the UK, everyone can invest up to £20,000 a year in an Individual Savings Account (ISA). Any interest accrued on these investments is tax-free for life, making them an incredibly efficient way to invest.

This limit renews annually, meaning you can contribute up to £20,000 each year. This is beyond the reach of many people, but you should try to maximize as much as you can on this tax-free investment vehicle.

Again, the U.S. has a similar vehicle called an Individual Retirement Account (IRA). There are two main types – traditional IRAs and Roth IRAs – which are similar but taxed differently.

Traditional IRAs allow you to deduct the amount contributed from your pre-tax income. The advantage here is that you defer your tax payments until later in life when you retire, a point in life where most people earn less (and therefore pay less tax).

The US is less generous in these vehicles than the UK, with the annual limit set at $6,000 ($7,000 for those over 50). This would be the personal investment vehicle of choice for most Americans.

Canadians have a similar vehicle called a Registered Retirement Savings Plan (RRSP) that allows participants to contribute up to 18% of earned income up to a maximum of $26,500. Canadians also have access to a TFSA (Tax-Free Savings Account) which allows you to contribute $6,000 a year as of 2022.

These types of accounts, with their favorable tax advantages, should be maximized alongside workplace pensions to build up sufficient retirement funds for a comfortable life post-retirement.

Whereas pension plans are automatically managed by your company’s pension provider, individual tax-advantaged investments need to be managed by you. This leaves many (understandably) overwhelmed as to where to invest their money once inside these tax-efficient vehicles.

Most of us are not experts in the stock market, and therefore rightly stay away from it. There is one investment vehicle, however, that is extremely safe and offers one of the best compromises of risk vs. reward on the market – Index funds.

Index-Funds: The Fundamental Investment Vehicle

Index funds have gained massive traction in the last few years as amateur investors, such as myself, have realized that they offer the most reliably safe return on investment in the stock market.

They are now so popular that as of 2019, more money is invested in passive funds (such as index funds) than in active funds in the United States. An index is a measurement of a section of the stock market.

For example, the most popular US indexes are the S&P 500, which contains the 500 largest companies in the US economy weighted by market capitalization, and the Dow Jones Industrial Average, a collection of 30 companies selected to represent their respective industries.

An index fund, therefore, sets to mimic the entire index. For example, buying an index fund of the S&P 500 will buy a little piece of (almost) every company in that index. Your results will therefore follow the index (almost) exactly, meaning you perform no worse or better than it does.

Since the S&P 500’s inception in 1957, the index has averaged an annual return of 8%. That is a pretty good return for minimal risk. There is no reason to believe this return won’t continue for the next 60 years.

The Benefits of Index Funds

Index funds have numerous advantages over types of investment vehicles. Firstly, they are about as safe a position as you can hold in the stock market, as long as your investment window is long-term (decades) which it should be (remember investment principle number 3).

Whereas individual stocks are highly volatile and susceptible to complete loss, index funds spread your bets across hundreds of companies.

Index funds track the index they follow, meaning the only way to lose your money is if the stock market completely collapses.

The only realistic way for this to happen is through the total collapse of the financial system, such as the total annihilation of the U.S. through war or a natural pandemic. In this situation, you would have substantially greater problems than your retirement savings.

Index funds are passive and take a set-and-forget type approach. You simply set up a monthly contribution to your find of choice, forget about it, and let time and compound interest do the hard work for you. Remember, we are investing for the long term, ideally decades.

The stock market, and hence your index fund, will ebb and flow with the financial tides, but the long-term results will mirror the average rise of its respective index for a historical average of between 7 and 9%.

Some years you may lose 20%, others you may gain 20%. Even if your index fund is down 50%, the power of compounding will allow it to grow, just at a lesser rate.

You don’t need to allocate any time or effort to maintain your investments, you simply need to open an account, pick your index fund, set up a monthly transfer, and collect your (hopefully) large pile of cash at retirement.

Passive Vs. Active Funds

The battle is now heating up between passive funds, such as index funds, and actively managed funds, such as the typical mutual funds, where you hand over your money to investment experts who handpick their own set of stocks using years of “insider knowledge” and “expertise”.

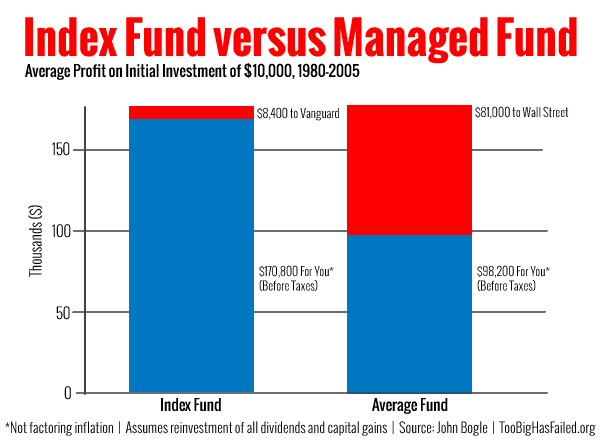

While managed funds can be more profitable short term (if you are lucky), long-term trends show index funds to be more profitable. 2019 marked the 9th consecutive year that the majority (64%) of actively managed funds lagged behind the S&P 500.

After ten years, 85% of actively managed funds underperformed the S&P 500, and after 15 years, nearly 92% trailed the index. This gap increases the longer the time span. In our ideal holding period (decades), the chances of an active fund outperforming a passive index fund tend toward zero.

What’s more, fund managers require fees of up to 1%. Passive index funds, on the other hand, require little maintenance, and fees can be as low as 0.1%. This seemingly small difference can result in tens of thousands once compounded over many years.

The most popular index fund in the U.S. is the Vanguard 500 Index (VFINX) which has an expense ratio of just 0.14%, and the minimum initial investment is $3,000. The Schwab S&P 500 Index (SWPPX) is another popular choice and performs much the same.

These can be purchased through investment platforms open to anyone, such as Fidelity, Charles Schwab, and E*Trade. Look for whichever platform has the lowest fees. Each country will have its own investment platform and index fund, so research the best platforms for your specific geography.

Remember to open these index funds in whatever tax-efficient account your country offers. For the U.S. these would be IRAs, for Canada, they would be RRSPs and TFSAs, and for the UK, ISAs. Aim to maximize these annual contribution limits as much as possible.

Conclusion

These basic principles should form the frontline of your saving and investing options. If you are canny enough to max them all out, you are ready to diversify into other investment vehicles, such as property and investing in businesses.

Even if you can only contribute just $50 or $100 a month towards these, they will leave you in a much healthier financial position than most. One of the best advantages is that they are all passive; you just set up an automatic monthly transfer and forget about them until retirement. From here, time and compound interest do all the hard work for you.

Let me know how it’s going for you in the comments below!

Intelligence Is Linked To Success, But Your Persistence Is More Important

While Intelligence is linked to success, it is genetic and cannot be significantly improved. Persistence, therefore, is what we must focus on.

The Subconscious Mind – What Is A Subconscious?

The subconscious mind has long been surrounded by mystery, but cognitive sciences are unravelling the mystery.

Habits Are The Foundation Of Success

Knowledge is not power without action, and habits form the consistent actions that compound over time to guarantee success.

Feeling Overwhelmed? Regain Control With These Simple Tips

Modern life can quickly leave you feeling overwhelmed if you are not prepared. Learn how to overcome these feelings and stay in control of your time

The Impact of Cannabis Use on Brain Function and Cognitive Performance

Discover The Impact of Cannabis Use on Brain Function and Cognitive Performance, exploring how heavy and moderate cannabis use affects memory, brain activation, and cognitive abilities.

The 7 Secret Benefits of Exercise

We all know exercise builds strength and reduces fat, but here are 7 more life-changing benefits and the types of exercise that best promote them.